MayDay @The FED?

What’s behind the numbers?

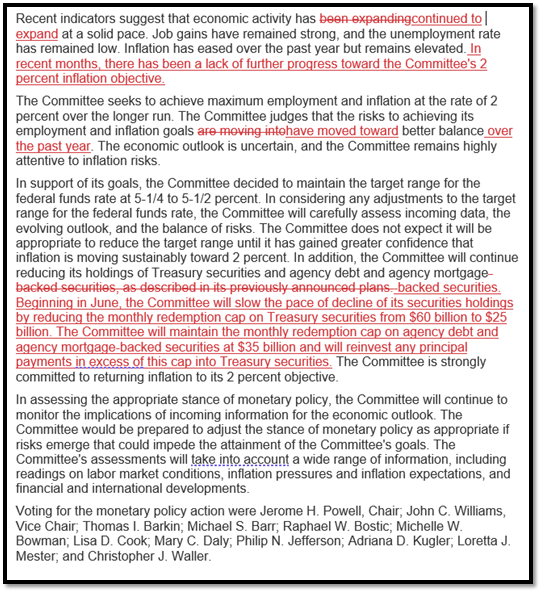

The Federal Reserve held interest rates steady for a sixth consecutive meeting at 5.25-5.50%, in line with expectations and market pricing.

In its press release, the FOMC added the following 2 sentences: ‘In recent months, there has been a lack of further progress toward the Committee's 2 percent inflation objective.’ ‘The Committee judges that the risks to achieving its employment and inflation goals have moved toward better balance over the past year.’

The most important announcement was related to the QT taper, which was bigger than expected. Beginning in June, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $60 billion to $25 billion. The Committee will maintain the monthly redemption cap on agency debt and agency mortgage-backed securities at $35 billion and will reinvest any principal payments in excess of this cap into Treasury securities.

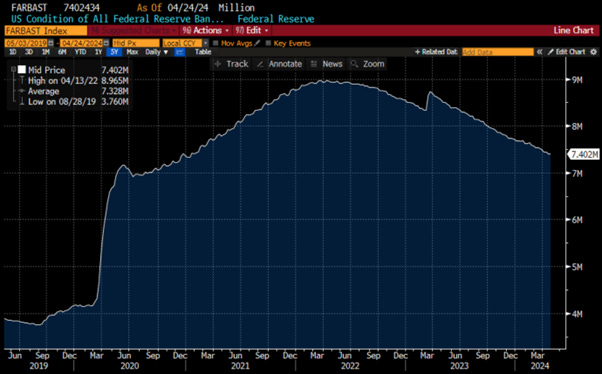

FED Balance sheet.

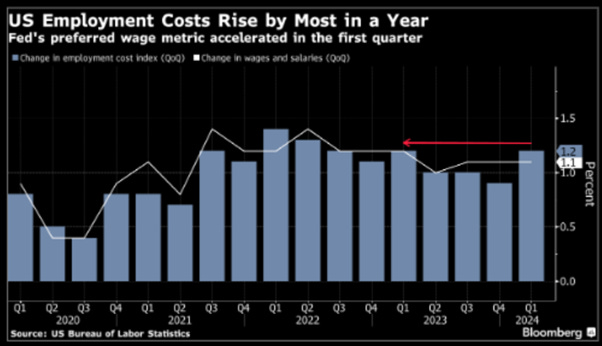

In his prepared comments, Powell reiterated that ‘inflation is still too high,’ while labor demand still exceeds the supply of available labor despite immigration as a factor in helping to boost the labor supply. He added that the committee has gained little confidence needed to lower interest rates, and this will take longer than previously expected.

During his press conference, Powell mentioned that ‘it is unlikely that the next policy move will be a rate hike’. To raise rates, the FED would need 'persuasive evidence' that policy is not tight enough.’ Asked about the rising risks of stagflation, in Powell’s opinion, ‘I don’t see the stag or the flation.’

Powell's opening remarks were mostly neutral; however, his comments over the press conference were relatively dovish as usual as he remains convinced that he will be able to bring back inflation to 2% before the Presidential election. However, this suggests that a pivot in June remains unlikely and that a cut later in 2024 remains ‘highly data-dependent’.

Thoughts.

The FED's decision to keep interest rates unchanged was widely anticipated.

The surprise is related to the size of the QT tapering, which, in plain English, means $105 billion gross issuance less needed in Q3, just ahead of the election, with the FED implicitly helping the US Treasury to finance its gargantuan fiscal policy, and indicating that long dated yields are too high ahead of the election.

The real question investors should start asking themselves is if the FED really matters to the real economy and investors' portfolios in the context of a gargantuan fiscal stimulus and a FED that has lost its independence from the political power represented by its ‘de-facto merger with Treasury’. The truth is, indeed, that the FED is as always behind the curve and has become highly political but not yet openly partisan.

Wall Street has been predicting rate cuts for almost two years and has been wrong every time. Economists were predicting a June rate cut a few weeks ago, and now investors are looking for September. September remains an 'open meeting,' but this assumes that the return of the inflation boomerang has eased by then, which is unlikely given the long list of supply chain constraints impacting the economy. Additionally, September is only 7 weeks before the Presidential election, and while the FED is a political apparatus, it may not want to appear clearly partisan ahead of this highly contested election. By November, if the geopolitical environment continues to deteriorate as it has been over the past months, the FED will likely look to a rate hike rather than a rate cut, even if Powell has dismissed that prospect for now.

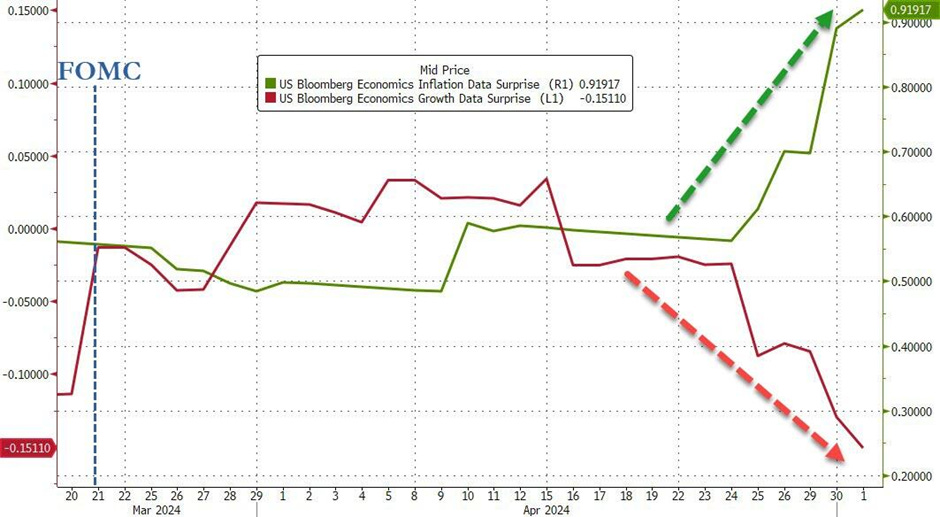

The market still eagerly anticipates a soft landing for the US economy, but over the past few weeks, signs have increasingly pointed towards the worst economic outcome Recession + Inflation = Stagflation. Indeed, even though Powell lectured investors that he 'doesn't see the stag or the 'flation' in markets, he should focus on how growth and inflation surprises have evolved since the March FOMC.

Anyone under the age of 60 has no real acquaintance with stagflation as the last time the US experienced such an economic scenario was between 1977 and 1981. This was a time of high volatility for equities and poor inflation adjusted returns.

And those who ignored hard assets like gold and were stuck in government bonds would have lost the attractiveness of the real antifragile asset in a period where investors lost confidence in government.

Performance of Bloomberg US Agg Index (blue line); Gold (red line) between 1977 and 1981.

Thoughts.

The FED's decision to keep interest rates unchanged was widely anticipated.

The surprise is related to the size of the QT tapering, which, in plain English, means $105 billion gross issuance less needed in Q3, just ahead of the election, with the FED implicitly helping the US Treasury to finance its gargantuan fiscal policy, and indicating that long dated yields are too high ahead of the election.

The real question investors should start asking themselves is if the FED really matters to the real economy and investors' portfolios in the context of a gargantuan fiscal stimulus and a FED that has lost its independence from the political power represented by its ‘de-facto merger with Treasury’. The truth is, indeed, that the FED is as always behind the curve and has become highly political but not yet openly partisan.

Wall Street has been predicting rate cuts for almost two years and has been wrong every time. Economists were predicting a June rate cut a few weeks ago, and now investors are looking for September. September remains an 'open meeting,' but this assumes that the return of the inflation boomerang has eased by then, which is unlikely given the long list of supply chain constraints impacting the economy. Additionally, September is only 7 weeks before the Presidential election, and while the FED is a political apparatus, it may not want to appear clearly partisan ahead of this highly contested election. By November, if the geopolitical environment continues to deteriorate as it has been over the past months, the FED will likely look to a rate hike rather than a rate cut, even if Powell has dismissed that prospect for now.

The market still eagerly anticipates a soft landing for the US economy, but over the past few weeks, signs have increasingly pointed towards the worst economic outcome Recession + Inflation = Stagflation. Indeed, even though Powell lectured investors that he 'doesn't see the stag or the 'flation' in markets, he should focus on how growth and inflation surprises have evolved since the March FOMC.

Anyone under the age of 60 has no real acquaintance with stagflation as the last time the US experienced such an economic scenario was between 1977 and 1981. This was a time of high volatility for equities and poor inflation adjusted returns.

Performance of Bloomberg US Agg Index (blue line); Gold (red line) between 1977 and 1981.

Read more and discover how to position your portfolio here: https://themacrobutler.substack.com/p/mayday-the-fed

At The Macro Butler, our mission is to leverage our macro views to provide actionable and investable recommendations to all types of investors. In this regard, we offer two types of portfolios to our paid clients.

The Macro Butler Long/Short Portfolio is a dynamic and trading portfolio designed to invest in individual securities, aligning with our strategic and tactical investment recommendations.

The Macro Butler Strategic Portfolio consists of 20 ETFs (long only) and serves as the foundation for a multi-asset portfolio that reflects our long-term macro views.

Investors interested in obtaining more information about the Macro Butler Long/Short and Strategic portfolios can contact us at info@themacrobutler.com.

Unlock Your Financial Success with the Macro Butler!

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence.